Bull or Bear: A Review of the Bright Health S-1

Note: this S-1 review was co-written with my friend, Ryan Russell. Stay tuned for more stuff from both of us soon!

TL;DR: Bright, which got its start in 2017 as an insurance startup in the individual / MA markets, has quickly cobbled together a mini-version of UHG focused on the individual consumer over the last 18 months. Like UHG, they’re now focused on controlling the entire value chain — payor, provider, and enablement. Bright’s approach should be able to win in markets targeting individual buyers (exchanges, MA, etc) and it stands to benefit from growth in those markets over time (i.e. continued growth of exchanges & MA and/or ICHRA taking off). However, Bright’s approach to growth via acquisition could create operational headaches that limit its ability to successfully scale local market approaches and undermine its ability to own the entire value chain and successfully attract providers into NeueHealth, disrupting the flywheel it has built.

Minneapolis-based insurance company Bright Health Group filed its S-1 this week, announcing its intent to go public. A Bloomberg report suggested a few weeks ago that Bright could seek to raise up to $1 billion in the IPO, and that its underwriters are seeking a valuation of north of $10 billion and potentially up to $20 billion.

Bright is the latest insure tech startup to go public over the last few months, following in the capital markets footsteps of Alignment, Clover, and Oscar. Clover and Oscar have struggled out of the gate, finding it hard to justify massive valuations as public markets have been disappointed by the amount of losses they’re sustaining (Oscar) and /or inability to hit projections (Clover).

Can Bright avoid this fate in its early days on the public markets? Let’s go through the Bright S-1 piece by piece — starting with the overall business, then diving into the operating divisions it is breaking out, before wrapping with how the markets might view a bull and a bear case.

Oh, and there’s a “Bull vs. Bear” poll at the end for anyone who wants to share their opinion on Bright with us (you can click the link here as well). We’d love to hear your perspective on Bright’s business and anything you’ve agreed / disagreed with in this S-1 Review. We’ll plan on aggregating and posting feedback as a follow-up to this.

Let’s dig in!

Bright Health Group Overview

Bright Health Group currently serves 623,000 insurance members across 14 states via its Bright HealthCare business unit. Bright launched back in 2017 as a narrow network play for the individual exchanges via a partnership with Centura Health in Colorado. Bright has been able to grow membership in the individual exchanges substantially over the past few years. It currently has 515,000 members across 11 states in its commercial health plans, which includes a small number of employer members, but is still predominantly individual membership.

In 2018, Bright entered the Medicare Advantage market with limited success attracting members via organic growth, reaching only ~6,000 as of 2021. Bright has focused its efforts more recently on growth via acquisition, acquiring two Medicare Advantage health plans in California that have increased its MA membership to ~108,000 today in total. It would appear that Bright has cracked the code for how to grow membership in the MA market, particularly when comparing it to other Medicare Advantage insurance startups, which have also languished trying to grow organically in the same. .

Perhaps most notably in the S-1, Bright introduces us to its new provider enablement platform business, NeueHealth, which is designed to help primary care practices move towards value based care contracts. Bright introduces Neue and its importance at the beginning of the Management Discussion & Analysis section of the S-1 by making this statement:

While Bright HealthCare is currently a larger contributor to revenue, due in part to the significant health plan premium revenue contribution from our consumers, we believe NeueHealth has a disproportional impact on our enterprise today and anticipate it will become increasingly important to our business and prospects, contributing an increasing percentage of our overall revenue in the long-term. We have presented NeueHealth first in the following discussion, consistent with management’s view of our business.

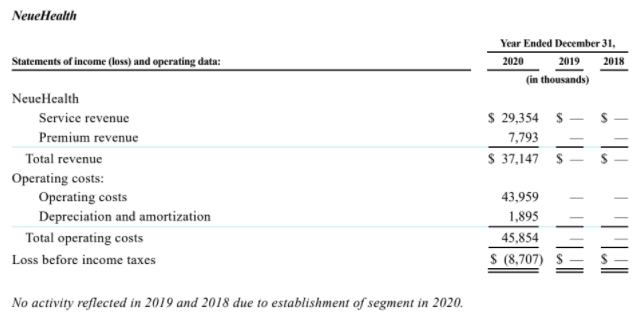

Yowza. That’s a big statement for a company that generates almost all of its revenue through Bright HealthCare, its core insurance arm that has 623,000 insurance members. Meanwhile, The Neue platform was just launched in 2020 on the heels of an acquisition of a provider group in Florida, and they’ve also acquired another Florida-based provider group more recently. Bright highlights in the S-1 that Neue is currently caring for 75,000 patients across 28 affiliated clinics and managing care at another 33 clinics, which appears to represent the business of the two provider groups it has acquired in Florida.

Yet even with those acquisitions, Neue only represented around 3% of Bright Health Group’s total revenue in 2020. Neue generated $37 million of revenue versus Bright HealthCare which generated $1.1 billion of revenue. And it’s worth noting that a chunk of the revenue Neue is generating is essentially an inter-company transfer between Bright’s operating segments as Neue is charging Bright HealthCare for renting its own provider network. So it appears the Neue revenue to date is basically that of the two primary care practices Bright acquired in the past year and an internal transfer. Given all that, Bright is taking a bold approach by separating Neue as a business unit from the very beginning of life as a public company, sending a strong signal to the markets that it views itself as more than just an insurer.

Conceptually, Neue is hitting on one of the hottest trends in healthcare innovation at the moment by helping primary care providers successfully manage risk. And this integrated payor / provider approach has the potential to be a key differentiator for Bright as it attempts to attract individual members to its insurance products, assuming that affiliated providers will push Bright’s insurance plans to patients. That is quite the flywheel if done successfully. The challenge in this approach is successfully threading the needle of attracting quality providers to become affiliated with Bright, particularly in this macro environment where every insurer / risk-bearing entity is pursuing a similar approach. While the acquisition of two groups in Florida is a good start down this path, it’s hardly evidence that Bright can successfully scale this approach over time.

All of these dynamics make Bright a rather interesting business to pull apart — you have a core individual exchange platform that has grown nicely, a MA platform that hasn’t grown organically but has benefitted from two bolt-on acquisitions, a PCP clinic business, and a MSO business for PCPs. That sure seems like a lot of different businesses to be building all at once.

One thing is quite apparent from looking at Bright’s general approach over the past few years—it is taking a page from the playbook of its big brother down the street, UnitedHealth Group. Let’s touch on those similarities for a bit.

Following in the Footsteps of UHG

Bright’s ties to UHG run deep as both founding CEO Bob Sheehy and current CEO Mike Mikan spent the majority of their careers in leadership roles at UHG. It is not surprising then to see Bright leaning in fully to the UHG playbook in a few regards:

- Breaking out the insurance business (UHC) versus the tech platform / services business (Optum). For years, UHG has been pushing the narrative that it shouldn’t be valued as a traditional insurer given its Optum business. Given UHG’s success going down this path, essentially every other insurer is attempting to go down a similar path of building a services business to capture better economics. Bright is rapidly moving down this path as well, even if Neue is still a nascent business. While most other insurance startups are also building their own platforms, Bright is unique in calling out Neue so early on as its own business unit.

- Growth via acquisition. UHG has never shied away from growth via acquisition. The entire UHG business has essentially been a series of acquisitions that have been pieced together over time. The logic seemingly has always been to generate cash flow from the insurance business and use that cash to acquire platforms that have reached scale, and generate more cash. Rinse and repeat.

Many startups in this space have taken the approach of needing to rebuild the entire healthcare / insurance stack internally over time, presumably coming from the perspective that healthcare is so irreparably broken it needs to be completely rebuilt. They shy away of acquiring incumbent plans or providers for fear of having to integrate with legacy systems and processes. Bright has taken a different tact, choosing to build and grow via acquisition, much more similar to the UHG model.

Heck, even the naming convention is oddly similar between the two organizations (Bright Health Group = UnitedHealth Group, Bright HealthCare = UnitedHealthcare, NeueHealth = OptumHealth). Wouldn’t it be wild if Bright acquired data analytics startups and a PBM over the next few years so it can add NeueInsight and NeueRx to the family? Ok ok we digress a bit.

Given UHG’s success with this general playbook, it makes a lot of sense that Bright is following in its footsteps. If Bright can carve out a position as a smaller, more nimble version of UHC + Optum, with more focus on the consumer at the localized level, it should be able to set itself up in a good position for continued growth. Of course, the one meaningful departure from UHG strategy is Bright’s willingness to sustain losses since its inception, but then again what health tech startup isn’t these days.

Bright’s Acquisitions:

As mentioned above Bright Health has pieced together a number of key aspects of its business via acquisition over the past few years. Let’s take a look at the key acquisitions featured in the S-1:

Insurance Acquisitions.

- Central Health Plan of California was acquired for $323.6 million in April 2021. Central Health Plan of California is a Medicare Advantage insurer that serves about 40,000 members in California. Central Health Plan also serves a few thousand dual eligible Medicare-Medicaid members, providing Bright with an initial entry into that market. Prior to the acquisition, Central Health was owned by a local hospital, Alhambra Hospital Medical Center, AHMC. As Bright noted in this recent interview, they were attracted by Central Health Plan’s focus on providing care to Asian and Latino American communities and plan to expand upon that model.

- Brand New Day, aka Universal Care, was acquired for $286.9 million in April 2020. This acquisition provided Bright with a Medicare Advantage plan in California with significant membership. Brand New Day had around 48,000 Medicare Advantage members mostly in California at the time, and has been growing membership nicely the past few years — 24% in 2020, 38% in 2019, and 112% in 2018.

- True Health New Mexico, a physician-led health plan in New Mexico focused on commercial markets, both individual and employer. Bright acquired True Health from Evolent Health in March 2021 for $27.5 million, $3.4 million net of cash acquired.

Provider Acquisitions.

- Premier Medical Associates of Florida (“PMA”) was acquired in December 2020. Bright acquired a 62% interest for $74.2 million. PMA is a multi-specialty practice that has 17 locations in central Florida focused on treating seniors, with some in the Villages, the source of many health care nerd’s favorite urban legend about senior health in this country.

- Associates in Family Practice of Broward, renamed AssociatesMD, was acquired at the end of 2019 for a total purchase price of $41.0 million. This acquisition appears to be the genesis of Neue, as Neue began reporting revenue in 2020. AssociatesMD has over 20 practices in the Miami area in Florida. It’s technically a multi-specialty practice as it has a handful of cardiologists, neurologists, etc, but it is heavily focused on primary care / urgent care.

Tech Platform Acquisitions.

- Zipnosis, a Minneapolis-based telehealth startup that has worked with health systems to provide a white-labeled telehealth platform, was acquired in March 2021 for $51.4 million, $48.2 million net of cash acquired. It appears that Bright has rebranded Zipnosis to DocSquad, which is a core part of the new tech platform that Bright is rolling out called BiOS (more on that below). This deal seems like an absolute steal for Bright. They were able to acquire a telehealth platform that has become a core piece of its S-1 story only a two months later for only $50 million as telehealth company valuations have gone through the roof.

Competition

As Bright has expanded its business from over the last several years, it has accumulated a very broad set of competitors that are highlighted in the S-1.

The NeueHealth segment competes with the companies you’d expect in the primary care enablement space — “MSOs, IPAs, and other organizational providers of primary care services, such as Agilon Health, ChenMed, Iora Health, Oak Street Health, OptumHealth, and VillageMD”. It is interesting to note how this competitive set is almost exclusively focused on primary care, particularly when considering that Bright’s Care Partners are generally health systems. It’s easy to read this as a shift in their strategy moving forward away from those health system partnerships and toward primary care relationships.

The Bright HealthCare segment competes with the companies you’d expect in the insurance market. They list “large, national insurers, such as Aetna, Anthem, Centene, Cigna, Humana, UnitedHealthcare and others”; “regionally-focused payors such as Blue Cross Blue Shield licensees, Kaiser Permanente and other provider-sponsored health plan organizations”; “and recent market entrants such as Alignment Healthcare, Clover Health, Devoted Health, Oscar Health and others.”

The breadth of this competitive set is impressive — from Agilon to Oak Street to OptumHealth to Kaiser to Anthem to Oscar — but also raises questions about how much Bright can expect to successfully accomplish at once when they’re competing with essentially every player out there at the nexus of payor / provider relationships.

Regardless of the breadth of comparisons, it will be difficult for Bright to escape the natural comparison to the class of insurance startups that have all gone public over the last few months — Bright, Clover, Oscar, and Alignment.

The Insurance Startups: Bright v Clover v Oscar v Alignment

While all these insuretech startups are coming to the public markets at very similar times, they’ve all come from different places:

- Bright started off focused on the individual market and growth via acquisition

- Oscar also focused on the individual market but has focused on rebuilding the entire experience internally

- Clover built a tech-forward MA plan out of a health system in NJ

- Alignment has focused on building a better MA plan

One notable similarity — beyond the significant losses each has incurred — between Bright, Clover, and Oscar is their insistence on being labeled as tech platforms with an insurance arm rather than an insurance company. Clover has played up it’s Clover Assistant platform as the core driver of the business, and Oscar just formally launched its +Oscar platform. It would seem they each think the public markets will be more willing to give them a pass for the massive losses if the companies are viewed as scalable tech platforms, where funding growth via losses is generally the norm.

Bright, perhaps with the benefit of having seen Clover and Oscar struggle in the public markets for a few months, has actually gone the furthest down this path of the three, splitting its business into two reportable segments, Bright HealthCare (the insurance co) and NeueHealth (the platform).

Bright’s Market Growth Strategy

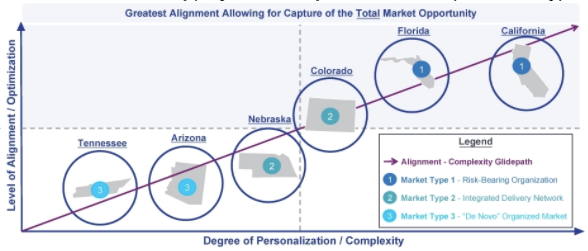

Bright takes an interesting point of view in terms of segmenting potential markets by potential alignment type with providers, breaking them down into three separate approaches:

- Markets with risk-bearing organizations. These are markets that have a strong presence of IPAs and MSOs that have aggregated physicians into risk-bearing organizations. Bright references Florida and California as examples of these markets. It is not surprising to see that Bright has acquired medical groups in Florida. You’d expect to see them pursue a similar approach in California as well.

- Markets with integrated delivery networks. These are markets that have IDNs that have invested in managing a network of clinically aligned physicians. Of course Bright’s relationship in Colorado with Centura Health is the leading example of this relationship.

- “De novo” organized markets. Basically these are markets that don’t have either of the above and Bright gets to help bring the market together.

Conceptually this framework makes sense, and it results in the nice 2x2 framework depicted in the S-1 as shown to the left here. But it doesn’t appear all that useful in terms of understanding what markets Bright might enter next, or how it will enter those markets.

For instance, Texas has to be high on their list of markets to enter next given the size of the individual market there. Presumably, they haven’t entered yet because they haven’t found the right partner in one of the Texas MSAs, which historically have been a hard markets to enter in the individual markets. If they could find a medical group to partner with, that seems like it would be the ideal partner for Bright, followed by an IDN that has invested in population health capabilities.

In other words, it would seem that Bright will place states on this map based on who they’ve been able to partner with in the state, instead of the other way around. The 2x2 does seem to indicate that Bright would prefer markets that have strong IPAs and MSOs, which makes sense given their general overall strategy. Bright is also clear to note, though, that it can expand into any of these market types and successfully manage medical spend in those markets.

While all of these approaches to growing into new markets appear valid, Bright’s willingness to take a unique approach in each market invites the question of ‘how effectively can Bright scale?’ into new markets given such localized efforts.

Bright HealthCare: The Insurance Business

Bright HealthCare represents the traditional insurance business inside of Bright. This part of the business isn’t overly complicated — it got its start back in 2017 as an insurer in the individual markets, entering Colorado via a partnership with Centura Health. Bright has also entered the employer market and the Medicare Advantage market. Lets take a look at each of those parts of the business.

The Commercial business. The majority of Bright’s growth to date has come from the commercial book of business. Prior to 2021, the commercial business was entirely individual exchange membership, which they have grown to 11 markets. In 2021, Bright began offering group membership to employers in addition to the individual membership. Unfortunately, the S-1 doesn’t disclose how much of 2021 commercial membership is group vs. individual (presumably there is very little membership just given the timing), nor does it give us a breakdown of membership by market. But the over 20x growth from 22k members in 2018 to 515k members in 2021 is impressive. It’s also impressive that Bright has been able to increase its individual market share in Colorado from 9% in 2017 to 34% in 2020. It will be interesting to see if Bright is able to sustain it’s growth in the individual market or if it begins to slow down as the ‘political tailwinds’ as mentioned in the S-1 drive other insurers re-enter the market and get more aggressive driving growth in the exchanges. This KFF report does a nice job highlighting the increase in competition within the ACA.

The Medicare Advantage business. Bright also began entering the Medicare Advantage markets in 2018, although has had limited success growing organically in those markets over the past four years. As of May, 2021 Bright’s organic business has attracted only ~6,000 Medicare Advantage members across ten states, which isn’t exactly jaw-dropping growth. Bright’s struggles to grow in the Medicare Advantage market aren’t exactly unique — most of the Medicare Advantage startups have similarly struggled.

But what has set Bright apart from the other new entrant MA insurers is its recognition that growth via acquisition appears to be a viable path forward in this market. In fact, not only is it viable, but it represents a financial arbitrage play that seems to be a good use of capital given the valuations that private markets are assessing to insurers at the moment. Bright was able to acquire Brand New Day, a Medicare Advantage plan in California with ~47,775 lives in 2020, for only $286.9 million. That equates to a purchase price of ~$6,000 per member of that plan. Bright was able to acquire Central Health Plan for $324 million, representing a purchase price of ~$8,000 per member for its 40,466 members. Both of those numbers are an order of magnitude lower than Clover’s valuation when it went public via SPAC in October, at which point it was being valued at roughly $65,000 per life covered (not surprisingly, that valuation has retreated a bit since). The acquisitions also represent a significantly lower valuation than the value per member Bright itself expects to go public at. At a $10 billion valuation — the low end of the range per that Bloomberg article referenced at the beginning of this post — Bright would be valued at ~$16,000 per life. And keep in mind the majority of those members are individual members which generally would be valued lower than Medicare Advantage members. So any acquisitions it can continue to make like Central Health Plan and Brand New Day to fold in members seems like a no brainer for Bright. Will be curious to watch just how many acquisition opportunities like this there are over time.

Financials

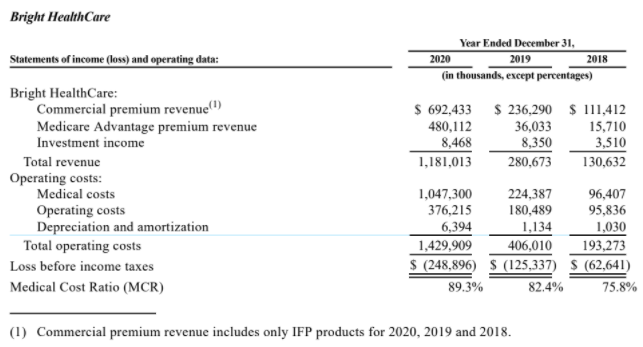

Bright, like every other insuretech startup, has burned through significant cash in its early years, with losses increasing to $249 million in 2020. The primary reason for this historically has been the operating expenses — if you look in 2018, for instance, it had an MCR of 75.8%, which is great for a startup insurer. The bad news is that MCRs have gone up substantially from 2018, to 82.4% in 2019 and 89.3% in 2020, at least in part due to new market entry. Presumably as Bright slows down its new market entry growth that MCR will begin moving in the right direction again, but it’s not great to see that trend. Bright’s operating expenses accounted for 73% of revenue back in 2018, which is… not quite as great as its MCR. The good news is that Bright has been able to get that down to 64% in 2019 and 32% in 2020, demonstrating what scale can do to spread those operating costs across a bigger denominator. Yet there’s still a significant way to go between that and the 12–15% range they are likely aiming to be at over the long term in order to get to profitability. This is likely to be one of the bigger challenges Bright faces in the eyes of public markets investors — whether it can make a turn towards profitability in the near future.

Bright HealthCare Proof Points

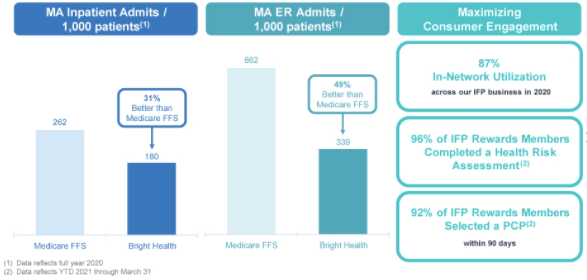

While Bright tells a good story about the overall business, it’s actually fairly light on details in the S-1. There is little discussion on what membership looks like by state or how the plan is working on the whole, which would be helpful in understanding the business. Bright shares the below chart as one example of their proof points. The MA data is great, but on a very small N (remember Bright had ~5,600 MA members in 2020 excluding Brand New Day membership) so it is hard to tell whether that is actually meaningful.

As an aside, has anyone ever seen a chart from a Medicare organization who hasn’t beaten the Medicare FFS benchmarks on inpatient or ER admits / 1,000 patients? It seems like every startup in the space right now cites this exact same data to prove how great their model is versus the Medicare FFS benchmark.

The other popular health insurance IPO metric pointed out is Bright’s NPS score of 78. That score is great, but, outside of the general skepticism around NPS as a valuable metric, there are several issues with it in this context: a) Every new “consumer driven” health insurance company touts a high NPS score, b) individual scores and industry averages vary widely, and c) each company does their own survey to obtain their score. Oscar and Clover both highlighted NPS scores of 30 and 59, respectively — so in absolute terms, Bright appears much more reference-able, but that doesn’t seem all that concrete.

Another important metric, especially in the individual markets, is YoY retention, which is not discussed in the S-1. The individual exchange is the wild west where most consumer decisions are made by plan pricing and/or influenced by brokers, who still assist on ~50% of individual enrollments and are still heavily incentivized by carriers. So a much better measure would be looking at NPS coupled with low churn to prove out a truly better consumer experience.

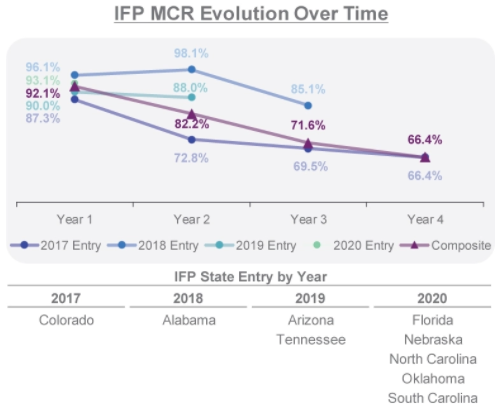

At the end of the day, though, the most important metric to follow will be how well Bright is managing medical expenses over time. And while they don’t share any data on the Medicare Advantage book of business, it does look as though they are managing MCR in the exchange book of business quite well based on this chart to the left. If they can continue performing in this manner while scaling the business to get operating costs down, it should put Bright in a good position to succeed.

Insurance Growth Opportunities

Bright has a number of opportunities to grow its insurance business within the Commercial and Medicare markets:

Group Market (ASO & Fully Insured). Most insurers start on one end of the spectrum of insurance product and move to expand into the other end. Bright is no different, moving into group fully insured and ASO from individual and MA. Ultimately, this will be another question of their ability to scale and ensure these different product offerings don’t become dilutive distractions. Both fully insured and ASO will require more focus on broker distribution resources and ASO, especially in the large market, is a different animal in terms of the sales cycle and customizations required. Another difference in the group market is many benefits folks will tell you their employees love the choice of broad networks — especially those who have already limited networks for cost savings. While they have PPO plans, Bright describes traditional choice networks as “broad, impersonal networks,” implying their narrow networks are more personal for the individual member. So those will be interesting conversations with employers — just not sure how much time Bright should be spending on them as it may be a tough space for them to gain traction in without detracting from the core business at this point.

Individual & MA. Bright’s focus on provider partnerships and acquisitions in the individual & MA markets should help them continue to grow efficiently in these markets targeting individual buyers. Other new entrants like Oscar must rely heavily on plan pricing, brokers (noted frequently in the Oscar S-1) and expensive marketing to grow membership — which is hard and not sticky given all of those things are fluid on a yearly basis based on aggressive competitive reactions that are different in each market. Outside of the previously discussed brokers, Bright is able to leverage the other key stakeholder that influences individual health plan decision making — the trusted provider. By partnering with and acquiring these trusted providers, the consumers being directed by these providers are going to be much stickier assuming the experience for both the consumer and provider doesn’t significantly deteriorate.

Direct Contracting. Bright shares in the S-1 that it has two Direct Contracting Entities (DCEs) approved for 1/1/2022 start dates. Of course, the Direct Contracting program has been under some scrutiny recently as CMS has decided to close the program to new applicants, but conceptually it represents a very interesting opportunity for Bright’s Neue platform as it seeks to move PCPs to more risk-based arrangements. It is curious to see that they chose to defer its start in the program until 2022. It would be interested to know how that decision was made internally knowing they were prepping for an IPO this summer and the bump that could have represented for NeueHealth revenue. This seems like something the Bright team would have jumped at given the size of Neue at the moment.

Medicaid / Duals. Bright currently operates in the Managed Medicaid space in California via its acquisitions there, and it notes in the S-1 that it believes it is well positioned to support the population in the future. Anticipate conversations about dual-eligible populations on future earnings calls.

ICHRA. Assuming ICHRA (an Individual Coverage Health Reimbursement Arrangement), continues to gain momentum, Bright should be well positioned here by leveraging their local provider presence and individual market share to tap into small groups wanting to remove the burden of benefits admin. Also, as Bright indicated they are pursuing fully insured group plans, they should be able to leverage both their existing provider relationships and the broker relationships they’ll need to develop in the group market to start offering a menu of options that can serve small groups who are on different stages of the risk adoption curve.

NeueHealth: The Provider Enablement Platform

NeueHealth is the new business unit Bright introduces in the S-1 that represents its recent extension into the provider enablement space. It’s worth mentioning again here that Neue only started generating revenue in 2020, and contributes only ~3% of Bright’s total revenue at this point. So while Neue is front and center in Bright’s S-1, the reality of the business today appears that it’s very early on. Neue’s website is currently a nicely-designed landing page, which adds to that feeling.

Neue started generating revenue in 2020, primarily as the result of Bright’s two acquisitions of primary care groups in Florida — AssociatesMD and PMA. Those two acquisitions appear to have formed the basis for Neue’s 28 risk-bearing primary care clinics. In those 28 directly managed and affiliated clinics, Neue provides care for 75,000 unique patients, of which 30,000 are in value-based arrangements with multiple payors today. Unfortunately Bright doesn’t share many details on this, but it is worth keeping an eye on how many of these patients they can flip to Bright insurance over time.

You’d assume that Bright will continue acquiring medical groups in this manner and will house them in this part of the organization. It will be interesting to watch if Bright ever chooses to build clinics on its own — or attempts to acquire one of the venture-backed Medicare Advantage clinic models.

Beyond the two primary care practices, it appears that Bright has decided to house all of its relationships with Care Partners — the IDNs it has formed narrow network partnerships with — in Neue as well. This allows Neue to generate revenue by charging Bright HealthCare for renting its network back to itself — essentially creating an inter-company transfer that makes revenue look higher for Bright Health Group. Bright notes in the S-1 that Neue revenue increased by $8.1 million in Q1 2021 over Q1 2020, “primarily driven by increased intercompany network contract service revenue with our Bright HealthCare segment, which is charged on a per consumer per month basis and has increased due to market expansion and an increase in consumers.”

It is interesting to see the way Bright handles its Care Partners in the S-1, given how the organization got its start building narrow networks in conjunction with Care Partners. Bright opaquely references that Neue is contracted with over 200,000 providers, which must be via Care Partner relationships. It’s odd to see Bright not discuss specifics of Care Partner relationships more in the S-1, which might indicate they have struggled to figure out a standard way of working with IDNs that can be easily described in the S-1. While it isn’t necessarily problematic that each IDN relationship is unique, it does present some potential complications when trying to scale those relationships in a repeatable way across markets.

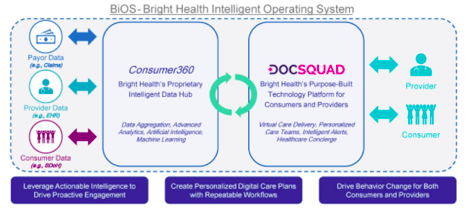

Lastly, Neue is also building a ‘Value Services Organization’, which appears to be their branded version of an MSO. This part of Neue currently manages care for 33 clinics, focused on supporting primary care practices to move towards risk-based contracts. This group seems to form the core of the provider enablement play, although there is not much detail in the S-1 on how it actually works so it’s hard to know what is going on here. Bright spends a good deal of time highlighting its BiOS technology platform as well as its DocSquad app, which presumably are a core part of its VSO services for providers. More on that shortly.

The biggest challenge with Neue certainly isn’t the concept — it is running a play that many other organizations in healthcare are also attempting in terms of moving care delivery orgs to risk-based contracts. The challenge is that Bright presents very little data in the S-1 to demonstrate that it can actually do any of this successfully.

Lets shift our sights now to the technology platform behind Neue, the Bright Health Intelligent Operating System, BiOS, to see what’s going on there.

The BiOS Technology Platform

Bright repeatedly references BiOS as a core part of its differentiated technology platform for both care delivery and insurance. Unfortunately, it shares very few details on the outcomes the platform is driving. This likely is because it doesn’t appear that this technology platform is fully deployed at the moment — Bright notes as much in its risk factors section: “We launched BiOS in 2021 and are in the process of making it fully operational with the completion of the rollout of DocSquad.”

Bright’s recent acquisition of Zipnosis appears to have formed the basis for DocSquad, so it makes sense they’re still rolling DocSquad out, given that the Zipnosis acquisition was only completed a few months ago. Bright somewhat randomly cites at one point in the S-1 that it has already completed 4 million virtual visits on the BiOS care platform. Yet that seems like a generous interpretation of what Bright has done versus what Zipnosis had done prior to being acquired. The number appears to include Zipnosis’s historical virtual visits, as Zipnosis cited having 2 million visits in 2020.

It creates some worry about the state of Bright’s technology platform that a small acquisition of a telehealth platform two months ago is forming the basis for their ability to build an ‘intelligent operating system’ that is at the core of the organization’s success.

It feels as though there is still a lot of work left to be done here, and it wouldn’t be surprising to see them make additional acquisitions here to round out their capabilities given the general approach Bright has taken historically.

It is worth noting that if BiOS can build this platform successfully, it feels a bit like the holy grail in payor / provider healthcare innovation — enabling a personalized consumer experience in healthcare that ties together the payor, provider and consumer platform all under one umbrella.

Financials

Given Neue is only 3% of revenue and one of the core customer’s is Bright itself, there isn’t really much to assess in the S-1 from financial or proof point perspective yet. There is a long ways to go in turning this business from two acquired primary care groups to a tech platform supporting primary care providers in managing risk-based contracts. It’ll be interesting to watch Bright try to grow this business over time.

In Summary

Bright Health Group’s S-1 certainly makes for an interesting story as the business has rapidly expanded over the last eighteen months. Bright’s core value and growth to date has been from it’s individual and MA insurance business, but it certainly tries to put its new platform segment front and center. Lets summarize the two key parts of the business:

Bright HealthCare — the core insurance business:

- Strong historical growth through market expansion and acquisitions in both the individual and MA space

- Variety of future growth opportunities continuing to follow the same playbook and riding tailwinds for other markets like ICHRA

- However, competition is likely to increase in the individual market and to be seen whether expansion into the group market will prove to be a distraction

NeueHealth —the provider enablement platform:

- An important piece of Bright’s flywheel to help them scale with local providers and consumers over time but it is unproven at this point at 3% of revenue and leveraging itself as a core customer

- Competition in the enablement space is increasing rapidly and it will be a arms race to partner with the best providers in each local market

- The technology platform intending to power this business is still being built in real time

- Hard to justify any sustainable advantage in this portion of business at this time but has the ability to effectively connect the payor, providers and consumers if it works

The Bull vs Bear Case

The Bull Case:

Bright will find massive success building the next big health care platform focused on coordinating insurance and care delivery around the individual consumer at the local level.

Bright has followed in the footsteps of the organization that has changed the playbook in healthcare, UHG, as well as anyone. Bright has demonstrated that it is adept at identifying and acquiring assets on the insurance and care delivery side that will help it achieve scale in markets faster than other new entrants to the insurance market (Oscar and Clover). And in health insurance and care delivery, scale is the name of the game. Once you reach scale, that gives you time to figure out everything else. Bright recognizes that in order to both effectively partner with providers and serve consumers where they are, you need to be able to adapt and be flexible to the needs of the local markets. It has honed its approach to meet the needs of those providers. This allows Bright to effectively partner with leading providers in local markets via Neue, which will help drive more members to Bright HealthCare’s insurance products over time. This growth pattern creates a flywheel that will be hard to stop once Bright achieves scale in a market.

The Bear Case:

Bright hasn’t developed any core competencies aside from being an effective acquirer of assets, and eventually this will cause Bright to languish as it struggles to digest, integrate, and find new partners.

While Bright has demonstrated impressive growth thus far, what have they really done other than efficiently deploy capital to acquire a handful of different assets? The S-1 is very light on details for anything aside from its experience in the individual exchange business. This is not surprising as essentially everything else Bright mentions has been acquired in the past 18 months — including the majority of its Medicare Advantage business, its primary care clinics, and its technology platform. While the idea they’re after appears to be the right one, Bright will fail to achieve its lofty aspirations, as it fails to integrate its acquisitions effectively. Leading providers in local markets will balk at joining Bright via Neue and instead choose other partners, which in turn will undermine Bright HealthCare’s insurance business. Bright Health Group will stagnate as it struggles to digest the various acquisitions it has made and attempts to clarify what its core competencies are as an organization.

Your Turn: Tell Us What You Think!

Ok — now that you’ve read through 6,000+ words of our thoughts on the Bright S-1, it’s time for you to share your thoughts on Bright with us here. Are you more bullish or bearish on Bright at this point? What did we get right or wrong in this analysis? We’ll aggregate responses and post any interesting ones as a follow-up to this post.