A Review of the Clover SPAC

GROWTH * GROWTH * GROWTH or SELL * SELL * SELL?

Clover, one of the Medicare Advantage insurance startups, announced on Tuesday that is going public via a SPAC owned by Chamath Palihapitiya of Facebook-fame at a $3.7 billion valuation. It’s obviously a great exit for everyone associated with Clover, but you’ll have to forgive me if I’m a bit befuddled that a 3-star Medicare Advantage plan with an MLR of 98.8% in 2019 and ~57,000 lives is somehow being valued at $3.7 billion (roughly equaling $65k per life covered). Granted, building up a Medicare Advantage plan to 57,000 lives is no easy feat. But a $3.7 billion valuation?

The valuation just doesn’t make a ton of sense if you’re just looking at this as a Medicare Advantage insurance company. Of course, Clover isn’t just being pitched as an MA insurer, it’s being pitched as a technology company that’s going to fix the healthcare space. A big part of the growth story discussed in the investor presentation, even though it’s not baked into the financials yet, is about the tech platform — the Clover Assistant.

It doesn’t help any of this that the investor deck could best be described as a hot mess. There’s very little detail on the business, and details that are there are at best confusing to understand. Here’s a link to the investor presentation.

Clover certainly doesn’t describe itself as two different businesses, but the valuation certainly seems to imply it. I’d have hoped that the investor presentation would have provided a bit more confidence that Clover is worth the astronomical valuation. But instead, the presentation seems to mislead the reader as to the current state of the business. More on this below. All of this has me yearning for the rigor of a traditional S-1 and IPO process.

As I’ve perused the deck, I’ve reached the conclusion that Clover is really pitching two separate businesses, with the second one driving the valuation upside:

- Clover, the Medicare Advantage plan

- Clover Assistant, the PCP technology platform enabling Direct Contracting

Let’s start digging into the business, first with some general context / background, and then going into the two seemingly separate parts of the business — the MA plan and the tech platform.

Some General Context

Beyond the dynamics of each part of the business that I’ll get into below, there are some worrying dynamics around this deal as a general context for the business. I’m a bit leery about this SPAC for a few reasons:

- In Vivek Garipalli, Clover’s CEO, you have someone who has legislators in his home state poking around an investigation into shenanigans related to him and others while they received over $150 million in management fees running Carepoint Health, the group of hospitals he ran prior to starting Clover. His legacy at Carepoint, by the way, was purchasing it out of bankruptcy and turning it around by going out of network with insurers and jacking up prices to turn a profit. In 2013 one of his hospitals was the most expensive in the country. Gross.

- In Palihapitiya, you have a guy taking full advantage of the zero interest rate environment and launching SPACs left and right. He is apparently launching a personal collection of 26 SPACs, which he is labeling IPOA to IPOZ. Clover, being the third of his 26 SPACs has earned the moniker of is IPOC. I am sure he is going to make a whole lot of money off his SPACs, but I’m a bit skeptical about the general societal value of whats going on here. Palihapitiya, fresh off his IPOC / Clover investor presentation show (more on that below) is already on to SPACs IPOD, IPOE, and IPOF. That leaves him twenty more SPACs to get through after that. He gets to benefit from taking companies public without the diligence of a traditional IPO process — or really any process at all — but where is the diligence and rigor on these investments for the general investor? His presentation on Clover is *at best* misleading, as we’ll get to below. Yet… he waves his magic wand and this all of a sudden Clover is worth $3.7 billion because the Virgin Galactic SPAC worked out?

- In Clover, you have a company that has a checkered past and widely missed the mark a number of times, including being fined by CMS for misleading marketing practices, pissing off its customers, and finally acknowledging it needed to hire more healthcare folks while laying off 25% of staff in 2019.

Clover, mind you, was pitching early on (presumably 2015) that it would have 65,000 Medicare Advantage members and a gross margin of 20% back in 2017. It has 57,000 MA members today, in 2020. It’s gross margin was 2.5% in 2019. I recognize that every startup is going to have its fair share of hard moments and you can’t always expect them to hit every project or number (and frankly getting to 57k MA members is a huge accomplishment for a lot of folks at Clover, who I’m sure have worked really hard to get Clover to this point). But… this seems like a bit more than your typical set of startup issues here. There is a pattern of behavior.

All of this seems like a recipe for general chicanery.

Adding to the sense of chicanery is that Palihapitiya’s portion of the investor presentation felt a bit like an imaginary episode of Silicon Valley where Erlich Bachman gave a TEDTalk on why healthcare is so screwed up in this country. If you aren’t aware already that healthcare is screwed up, it’s worth checking out. But if you already are aware that healthcare is screwed up… I’d just go ahead and skip the first 64 pages of the presentation. The slides are full of brilliant nonsense like slide #59, pasted below, which depicts why Palihapitiya is excited about Clover. It’s almost as though this dude ran growth at Facebook or something.

Soooo… this is the type of in depth analysis that gets a company public these days? Ok sweet deal I’m in!

Palihapitiya, to his credit, also tweeted a one-pager on his investment thesis for the deal, which is quite nice in it’s simplicity. Healthcare Industry = screwed up. Awesome Clover Tech = the solution. MA = big market. Clover = GROWTH * GROWTH * GROWTH. It’s worth reading if you’re interested in the thesis here.

All of this context makes me a little nervous about this deal and whats really going on behind the scenes here. Not to say that Clover can’t still be a great company despite some of the issues articulated above. But, I’d want to see some proof of that in the investor presentation before buying in. Unfortunately, this is where things seem to fall apart. Let’s check out Clover the Medicare Advantage insurance startup…

Clover: The Medicare Advantage Plan

Now we’re through the general context setting, let’s take a look at the mechanics of Clover’s core business as a Medicare Advantage plan.

Star Ratings.

Clover is a 3 Star Medicare Advantage plan. For context… while it technically is defined as an ‘average’ rating, that is not a good rating. If you worked at UHG and were in charge of a 3 Star plan I’m fairly certain that it would get you fired for gross incompetence. (I’m… only partly joking. You’d definitely get fired.). For reference, of the 410 entities that have MA contracts for 2020, 210 of them are at least 4 Stars, and 360 had at least 3.5 Stars. That means that Clover is in the bottom 13% of all Medicare Advantage plans on its Star rating, despite all of the cool AI technology. Perhaps it’s not surprising that Clover’s Star rating is not mentioned in the investor deck once. Ohhhhhh right, I forgot it’s a technology company, not an insurance company and AI algorithms will figure out how to fix that byzantine healthcare stuff later. No need to worry.

For those who aren’t aware, the Star rating is a pretty enormous deal for insurers as it is basically the driving force behind Medicare Advantage plan profitability. You have a good Star rating, you’re profitable. You have a bad Star rating, you’re not profitable. This is in large part because Medicare gives you pretty sizable bonus payments if you’re at 4 Stars or above as a plan. As this article suggests, an increase from 3 to 4 Stars can increase a plans revenue by ~15% as well as a 8% — 12% increase in enrollment. That… seems important, no? Maybe you should at least mention your plans to improve your Star rating in your investor deck?

Clover’s Growth.

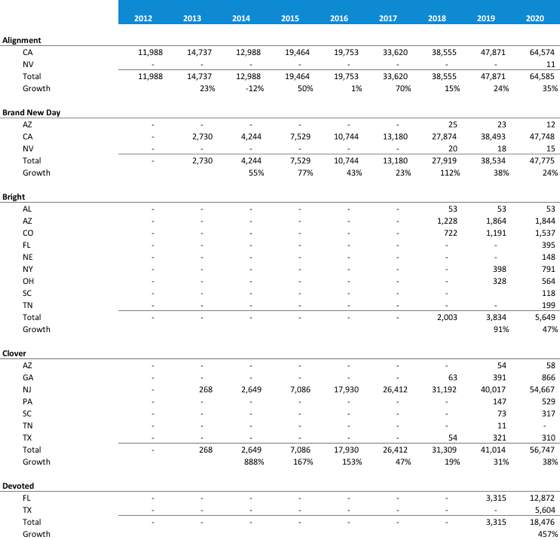

Referenced a few times in the investor presentation and by Clover folks is that Clover is the “fastest growing Medicare Advantage plan in the US (w/ at least 50K members)”. Leaving aside the mathematical game they’re playing to give Clover an advantage by defining the denominator as their membership number and no less (i.e. it excludes Devoted which had a significantly higher growth rate as it grew roughly the same number of members as Clover on a significantly lower base), let’s take a look at what Clover’s membership growth has looked like over time versus other Medicare Advantage startups:

Clover certainly does demonstrate solid year over year growth rates. And to be sure, growing in Medicare Advantage markets is really hard, as most healthcare companies find out. This blog post covers well the challenges of growth in the Medicare Advantage market for the startups in the space. It is not easy to demonstrate GROWTH * GROWTH * GROWTH in the space.

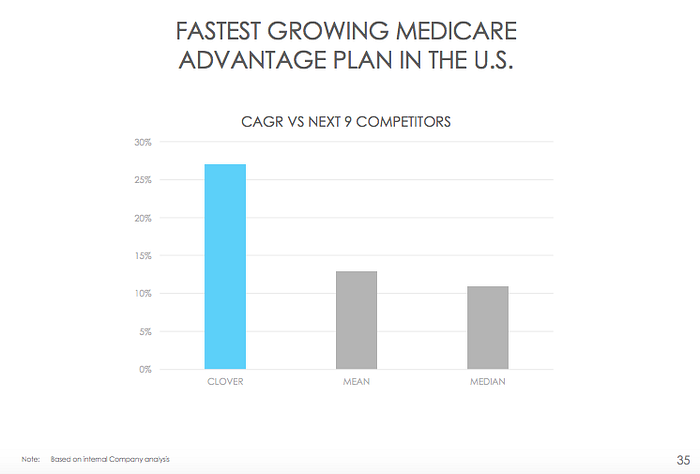

But at the same time, Clover’s growth seems pretty unremarkable compared to the other startups in the space. For instance Clover and Devoted both grew ~15k members between 2019 and 2020. And there’s not necessarily any problem with that — Clover is in good company with the companies on that list. But what I do take issue with is slides like this one below from Palihapitiya, referring to Clover’s growth rate as over double it’s next nine nearest competitors on average. Again, this all seems a bit disingenuous at best.

I’m really curious what Clover thinks its next nine competitors are here? It’d be helpful if Palihapitiya put some labels on these things.

Clover’s Market Share.

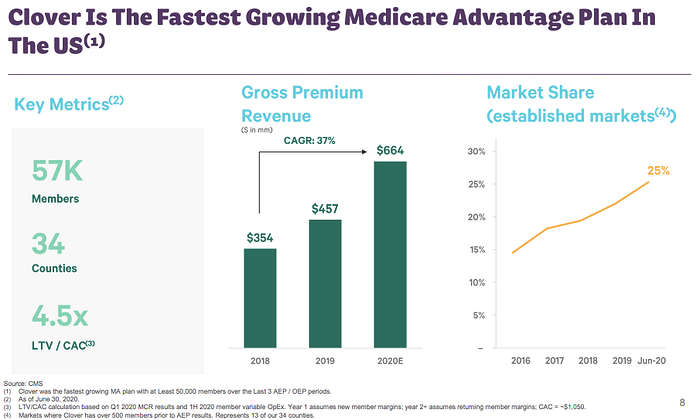

Clover presents a lot of numbers related to market share and growth that are misleading regarding its position in the Medicare Advantage market. For instance, check out slide 8 (slide 73 overall), which says in the title that Clover is the fastest growing MA plan in the US and talks about Clover’s market share being 25%, with the caveat that it’s only in established counties. Note also that Palihapitiya covered the market share data as well in slide 37, without any caveat about the 25% market share only in ‘established counties’.

If you look at that slide and think to yourself, jeez, Clover has an awesome business in the MA space, I wouldn’t blame you! 25% is an incredible market share! You’re in the neighborhood of UHC market penetration in that territory. That is really good. But then you check out the footnote and see that it’s only in counties that Clover has over 500 members… which I suppose has the benefit of being one way that you can look at market share? But if you look across Clover’s entire book of business… the market share story seems, well, a little bit different:

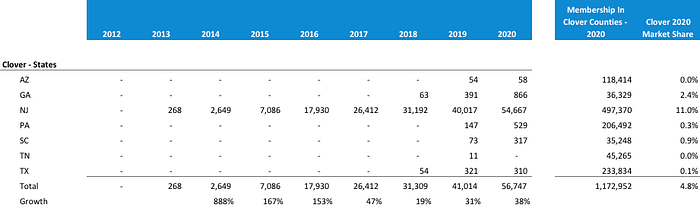

Clover hasn’t been able to reach 1,000 members in a single state outside of New Jersey. It has sub 1% marketshare in all of the states it is in aside from New Jersey, where it has 11.0% market share, and Georgia, where it has 2.4% market share. For a company that is supposedly in the GROWTH * GROWTH * GROWTH club, this seems a bit… underwhelming?

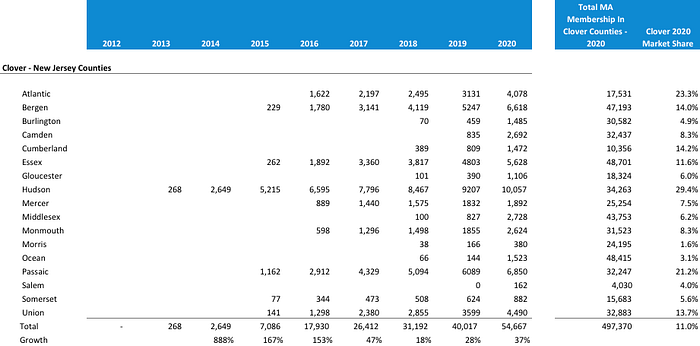

Even in New Jersey, Clover’s stronghold, it appears they’ve hit 25% market share in only one county—Hudson. That seems awfully different than their claims in the investor presentation. They’re above 20% market share in two additional counties, Atlantic and Passaic. Oh and by the way, those hospitals that Garipalli owned prior to Clover? Located in Hudson County.

Prior to 2016 it appears as though Garipalli was testing out Clover inside of CarePoint. While Clover was citing almost 7,200 members in 2015, while Clover’s insurance license wasn’t in the Medicare Advantage enrollment files in 2015. CarePoint Insurance Company, however, was in the MA enrollment files (for 2013–2015), and had right around 7,200 members in 2015. In 2016, CarePoint didn’t have any members. Garipalli seems to have built Clover on the back of CarePoint, making it a provider-sponsored plan of sorts in the New Jersey area. So it actually makes a ton of sense that they’re seeing a relatively good market share in Hudson — it is significantly easier to get people to enroll in MA plans when you have a friendly provider handy (note: this comes back into play when you think about Clover’s partnership with Walmart… it is one thing that could potentially kickstart some serious growth for them).

Clover had 56,747 total members in July 2020 across two insurance licenses (Clover HMO of New Jersey and Clover Insurance Company), with 54,867 of those members in New Jersey. In total, the counties where Clover had members had a total of 1,172,952 Medicare Advantage enrollees, meaning Clover’s overall market share is sub 5% across all of its markets. Let’s look at its market share even in New Jersey counties:

For all the talk about the advantages of technology driving growth and scale… it seems a bit worrisome to see how hard it has been for Clover to scale beyond a handful of counties in New Jersey. Check out the market penetration they have in some other metro areas that they’re offering product they’re in:

- San Antonio, TX. Clover has 247 members of 148,404. 0.2% share.

- Philadelphia, PA. 356 members of 123,649. 0.3% share.

- Charleston, SC. 183 members of 19,936. 0.9% share.

- Tucson, AZ. 48 members of 118,414. 0.05% share.

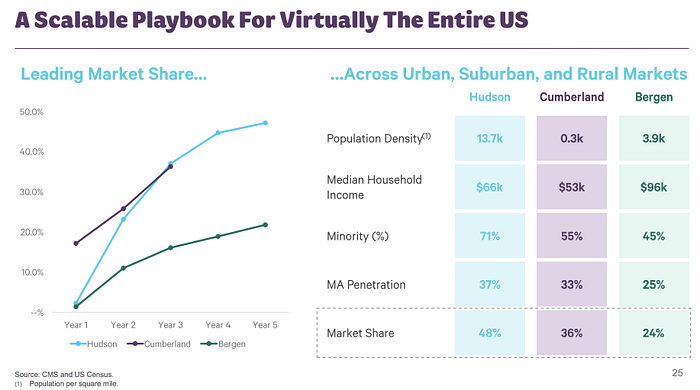

That’s… not great. Further confusing all of this is this slide below arguing that Clover has 48% market share in Hudson, 36% in Cumberland, and 24% in Bergen. Huh? As best I can tell that is demonstrably false given the CMS data above. Hudson is the highest market share at 29%, Cumberland and Bergen are 14%.

I am guessing that Clover is again pulling some slight of hand and referencing market capture — their share of net new members who are signing up for Medicare Advantage plans (Palihapitiya makes a comment along these lines on slide 36). Still… seems like they’re intentionally trying to cause confusion and make their market share rates look better than they really are here.

Also, if you look at the market share chart on the left side of the page on Slide 90 above, look at Year 2. Clover is saying all of those counties are above 10% in year 2. This is their ‘scalable playbook’, yes? **Goes and checks year 2 market share in markets outside of NJ in the charts above** Oh wait, the markets where they’re in year 2 of membership they have sub 1% marketshare. Turns out that scalable playbook seems like it still is yet to be written.

I believe ‘woof’ is the technical term for the current state of Clover’s market shares in new markets. It highlights how hard it is to acquire members in the Medicare Advantage market. This doesn’t strike me as the demand generation you’d see if Clover were akin to Tesla disrupting the car industry. It strikes me as the demand generation of a regional provider-sponsored plan that is trying to scale to new markets where it has no brand clout. Clover sounds much more like a regional Medicare Advantage plan in New Jersey at this point than a game changing technology company that’s in the GROWTH * GROWTH * GROWTH club.

To be clear, you can build a really, really nice business in the Medicare Advantage space without needing to make the claims that Clover is in the investor presentation. It turns out that even if you’re at 1% market share, it equates to hundreds of millions of revenue. You’ve just gotta manage the medical spend on that population effectively.

Brand New Day as a Comp

Somewhere in Minneapolis, the Bright Health team has gotta be laughing all the way to the bank on their Brand New Day acquisition earlier this year. Brand New Day is a California-centric Medicare Advantage plan with a 3.5 star Medicare Advantage plan (not perfect, but better than 3!) and has ~43,000 lives. Look at the growth trajectories of Brand New Day and Clover above and tell me you see a meaningful difference there — I don’t personally. You just have one high flying VC-backed technology startup and one sleepy old school healthcare company started in the 1980s, but got into the MA space at the same time as Clover.

Brand New Day, with its 43,000 members, is probably doing somewhere on the order of $430 million of revenue this year (43k members x $1k in premium per year). If they’re managing costs well, it certainly could be profitable on that book of business, and at the very least likely is not losing $200 million+ per year.

Given the Brand New Day acquisition was announced about a month after Bright raised $635 million, lets just go ahead and assume that Bright used all of the capital they raised to acquire Brand New Day (it doesn’t seem like it could have been any more than that or we would have heard about it in another press release). If anything that feels like the highest amount it could have been.

So, if you assume that Bright did pay a purchase price of $635 million, that would mean Bright paid ~$14,600 per Brand New Day member. This compares to Clover’s current valuation of… ~$65,000 per member. That strikes me as a particularly large difference, particularly while Clover is losing over $200 million a year. That tech platform sure is being valued pretty highly!

$635 million still seems like it’d be a great financial outcome for Brand New Day and the team there, although not quite the venture scale unicorn VC-backed startups feel the pressure to be. It also seems like a significantly more reasonably valued acquisition by Bright than by the SPAC — the difference in valuation per member is insane. Maybe we’re all just really good negotiators up here in Minneapolis or something.

Medical Cost Ratio.

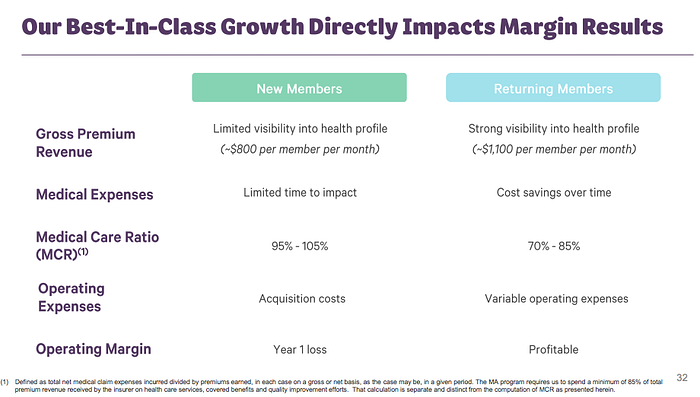

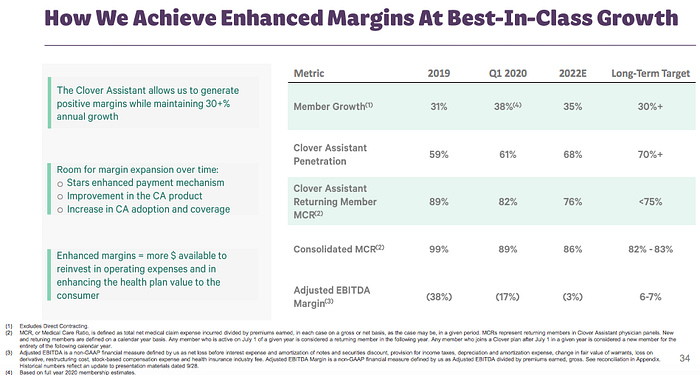

Clover spends a lot of time in its slides breaking down new members vs returning members, as they are significantly more profitable on returning members, which isn’t entirely surprising. Check out this slide on the financial breakdown between the two — note the revenue difference between year 1 and future years, which is a coy reference to the benefits of risk adjustment. Most notable is the wide gap in MCR. It drops from 95% — 105% in Year 1 to 70% — 85% for retained members.

Now, the 70% — 85% would be a great MCR number for Clover’s retained members… what evidence do they give to back up that claim? Turns out there’s next to nothing. Check out slide 99, which shows their ‘Clover Assistant Returning Member MCR’ at 89% in 2019. So… last year the MCR was 89% for Returning Members, but yet somehow Clover is going to get that to 70% — 85% for that same population? Ok.

Clover again generally displays some impressive sleight of hand with numbers like MCR throughout the deck. Their attempt to compare Q1 2020 data to 2019 full year data in the chart above is really deft, and obviously shows a nice decline from 89% to 82%. 82% would be pretty good for a full year, but the only issue with that analysis is that MLRs are always lowest in Q1 and generally go up throughout the year, with the highest being in Q4. Why not compare Q1 2019 to Q1 2020, Clover folks? Not exactly confidence inspiring. Maybe MCR will indeed come in at 83% for the year as Clover is predicting, which would be excellent — and given the year we’ve had with a pandemic, who knows! The data doesn’t exactly support it at this point though.

General Financials

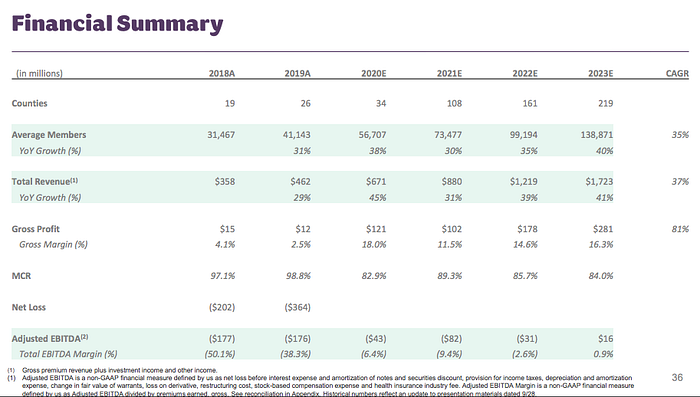

Clover only shares two years of historical financials in the slide deck, but those years aren’t pretty. Clover’s MCR for 2019 was 98.8% and 2018 was 97.1%. The company suffered net losses of $364 million in 2019 and $202 million in 2018. Note that according to reports, Clover lost $34 million in 2016 and $5 million in 2015. This is not exactly a confidence inspiring image.

Recap of Clover the MA Plan

To summarize all of this so far:

- Clover is in the bottom 13% of all Medicare Advantage for its Star ratings

- It only has meaningful marketshare in a handful of counties where its CEO used to own hospitals and started the plan as part of the hospitals

- It is not growing meaningfully anywhere outside of its stronghold counties in NJ

- It has a historical MLR running over 98%

- It is hemorrhaging cash, with over $200 million in losses each of the last two years

Clover’s Medicare Advantage plan feels like it is sinking and needs to start bailing water. No wonder they are placing so much weight on the pivot to Clover Assistant as a PCP enablement platform. On to that!

Clover Assistant: The PCP Tech Platform Enabling Direct Contracting

Throughout the investor presentation Clover and Palihapitiya talk up the Clover Assistant as the key driver behind the Clover platform and the tool that will drive its entry into Direct Contracting. The Clover Assistant is an AI software platform for PCPs that helps them drive patients to high quality, low cost care, and get them paid faster (and more?) for their Clover members. See Slide 80 for an overview.

Adoption of Clover Assistant

I am quite skeptical on the adoption of the Clover Assistant software based on the investor presentations. There are virtually no numbers anywhere in the deck on how many PCPs are actually using the Clover Assistant. The one meaningful number that appears in the presentation is on Slide 99 referenced above, where they cite that Clover Assistant Penetration is at 59%. Its a baffling number in many regards, but of course, because this is a SPAC there isn’t any context for what the numerator and denominator of that equation are. Penetration of what, exactly?

Conceptually, I have a really hard time understanding how the heck Clover is convincing PCPs to use Clover’s software platform, particularly in markets where they have <1% market share of the Medicare Advantage market. It baffles me. If you’ve never chatted with anyone at an insurance company about how fun it is to try to convince PCPs to use your software because it will help them improve care delivery, I’d suggest you have that conversation before you considering investing here. It is really hard to do with docs you’re friends with and have significant market share. It is nearly impossible to do at scale when you’re missing those elements. Heck, even one of Clovers early investors argued a point along these lines as well a few years back (in a really good read questioning MA startup insurance models in its own right).

So how in the world is Clover citing penetration around 59%? I’m not sure. If I had to guess, I’d guess it has something to do with relatively high penetration in New Jersey where they have existing relationships with the providers.

Now, it would seem this is where the Direct Contracting angle comes into play, because the one straight forward way to get PCPs to use your software is by convincing them it’ll make them more money.

Clover Assistant Outcomes

In theory, the Clover Assistant sounds quite cool as laid out in the slides — an AI platform that can drive better care at lower costs. Ok Sweet! I can see why Palihapitiya is excited! But again… I’m curious if any of this stuff is real at this point? If you have 59% penetration of the Clover Assistant, whatever that means, can you demonstrate **how** it is saving money for your members? The assumption that MCRs are going to drop from 89% last year to 76% by 2023 (Slide 99) for the Clover Assistant Returning Member population is a HUGE reduction. What’s the mechanism driving that cost savings? Lets check out a slide on this:

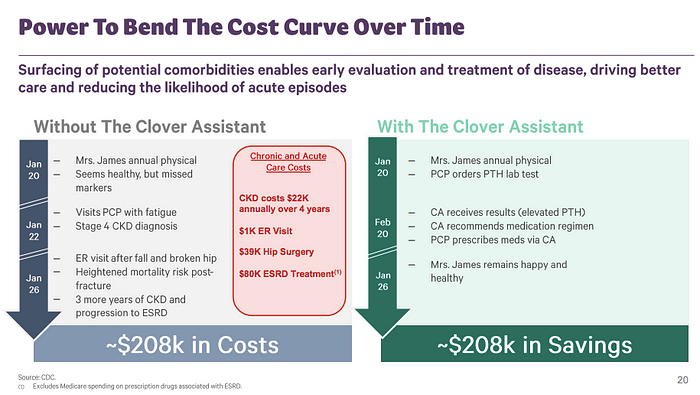

Wait… what? This is the slide Clover is using on how the Clover Assistant bends the cost curve? Despite having 59% penetration which would suggest they have some meaningful engagement with the platform? This slide reads like it came from the founders of a startup trying to get into a Y Combinator program after they stayed up all night reading academic papers on how software can bend the cost curve in healthcare.

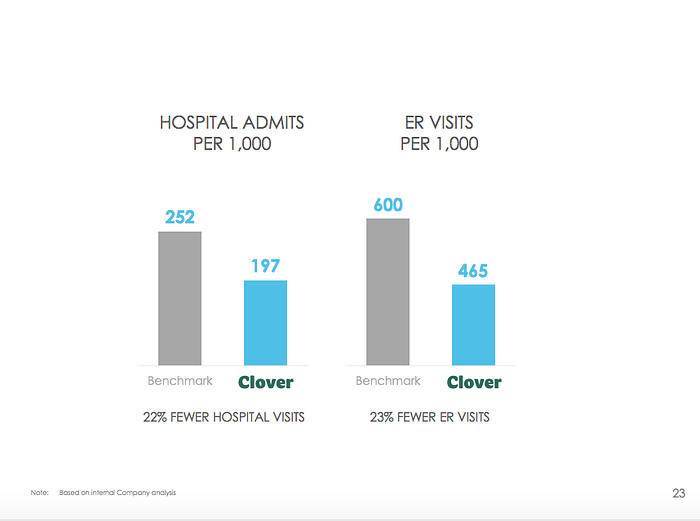

Palihapitiya at least shows some data on how Clover reduces ED utilization and hospital admits per 1,000… but what is this from? Is there a study they can share on it? Citing internal analysis without any additional context makes it essentially meaningless as shown in the slide below.

The Clover Assistant may very well do all of these things. But come on, is this seriously what Clover is putting out there as its going public at a $3.7 billion valuation? Conceptually I get the arguments they’re making. But… this is the justification for a public company of how the Clover Assistant is going to drive MCRs from 89% to 76%, when the Clover Assistant is already at 59% penetration and the MCRs aren’t there now? Give me a break.

The Direct Contracting Model

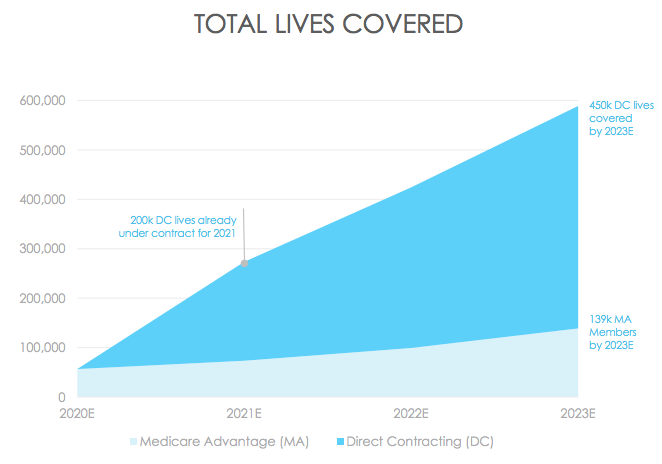

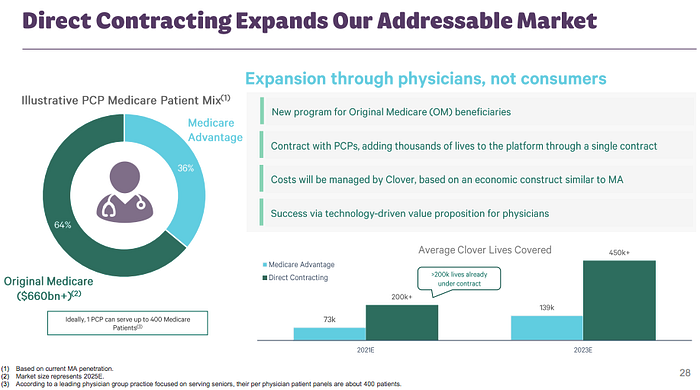

Ok, onto the lifeboat — the Direct Contracting play. Palihapitiya and Clover play up the Direct Contracting initiative from CMS as a key driver of future growth for the company. Clover says in the investor presentation that they already have 200k lives under contract for 2021 and expect to have 450k lives in 2023. Without much detail in the investor presentation, it’s really hard to know what they mean by this. It seems like a huge growth expectation placed on a nascent contracting strategy, although if it works it could pay off huge. The problem at this point, is there is no meaningful data in the investor presentation to suggest why they expect to have success in this market versus competition (and if Clover is expecting 450k lives in this space in the next three years… you can bet there will be competition).

It’s a rather large bet they’re placing on a Direct Contracting initiative, which mind you is still a CMS Innovation program that is just launching in 2021. The program appears to be generally designed around reducing costs in FFS Medicare by bringing some of the Medicare Advantage innovation into Medicare and enabling PCPs to take capitated payments. Given the success in the Medicare Advantage space, it’s not hard to envision a scenario where this model does take off (although, I continue to think the team at BCBS NC poked a very meaningful hole in the cost savings story of Medicare Advantage primary care models… i.e. they don’t).

Is Clover… an MSO?

What is particularly interesting about the Direct Contracting strategy for Clover is that it appears to be a major shift in customer base. Whereas with the Medicare Advantage plan they’re targeting seniors via D2C channels and competing against other Medicare Advantage insurers, in this model their customer becomes the PCP, and they’ll be competing against other software platforms for primary care groups. That is a really huge shift in corporate strategy for Clover, and one that seems to get washed over in the investor presentation a bit.

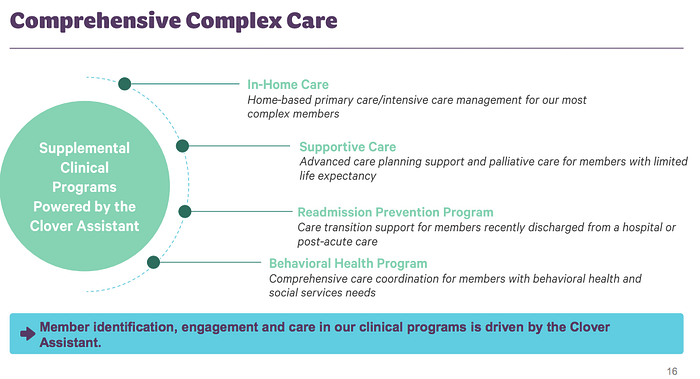

Even beyond that shift in target market, it sounds like the Clover Assistant product offering is akin to what an MSO organization would provide for PCPs. For instance, check out slide 81, which outlines the capabilities Clover Assistant is providing — in-home care, supportive care, behavioral health, readmission prevention. That sounds an awful lot like a suite of services an MSO would provide to PCPs, not all that dissimilar from what a VillageMD is up to.

Leaving aside the all of the questions related to the Medicare Advantage plan and how much of this actually exists today, I actually like the general approach here, particularly when you’re wrapping it in a Direct Contracting construct where you’re helping PCPs get paid. It would make a lot of sense that companies will find success doing this if the Direct Contracting model takes off. Will that company be Clover? Based on the investor deck I have no real reason to believe so. But Garipalli has demonstrated he knows how to be ahead of the curve on regulatory changes in healthcare, and perhaps he is again here.

Recap of Clover the Tech Platform for PCPs:

To summarize the Clover Assistant / Tech Platform / Direct Contracting session:

- Understanding current adoption of the Clover Assistant is sketchy at best

- There’s no real data supporting how Clover Assistant reduces medical spend

- Direct Contracting is an early but potentially meaningful regulatory change

- If Direct Contracting takes off, it seems plausible that companies supporting it will do very well

- Clover looks like its pivoting to an MSO model to chase this growth

It makes sense why Clover is chasing this opportunity, given all of the dynamics seemingly at play with the MA plan. There’s a huge, unproven, growth potential in the Direct Contracting market… we’ll see if Clover can execute on the shift.

Closing Thoughts

Whew — that was a lot. To take it back to the beginning, we’ve got Clover essentially acting like two companies in one:

- the D2C Medicare Advantage plan

- the B2B primary care tech platform

It sure sounds like an awful lot for any company to bite off when you look at it this way, let alone one that has had the very public missteps that Clover has had historically.

When you combine the challenges at hand with almost no data supporting the plans they’ve lay out, it again feels a bit like you’re watching an episode of Silicon Valley unfold, not looking at a $3.7 billion industry changing company. All of that said, if Garipalli has proven anything at CarePoint and Clover it is that he understands the impacts that regulatory changes can have on healthcare and if he sees Direct Contracting as a path forward, it is probably wise to keep that in mind. Perhaps he’ll be able to pull a rabbit out of a hat.

The Walmart partnership is something to watch with Clover going forward, as they could end up being something of a white knight in all this mess. Given all of the struggles Clover has had as a Medicare Advantage plan, I still cannot fathom what Walmart was thinking strategically when it picked Clover as its partner to get into bed with from a Medicare Advantage plan perspective. The technology mixed with the Direct Contracting play must have gotten them excited. Regardless of the reasoning, given that Walmart has decided to jump in with Clover, you could see that partnership opening a lot of doors for Clover to grow membership really fast, and clinics to use the Clover Assistant in, if Walmart chooses to expand the relationship quickly. I would still think that if Walmart goes that route, it would make more sense for them to acquire a Medicare Advantage plan (after all the entire premise is that Walmart’s brand is the one that will bring membership, which is the key challenge in the space). If that’s the case, it seems like the $3.7 billion valuation of Clover at the moment would be a hard pill to swallow here for Walmart. But its entirely possible that the partnership approach here works out for Clover and they use it to drive GROWTH * GROWTH * GROWTH.

As the SPAC was announced earlier this week, Garipalli was on Squawk Box the morning the deal was announced and shared that they had been running a formal IPO process as a parallel path to this deal, and had filed an S-1 as part of that. It sounds like the SPAC approach came in at a higher valuation that would have been hard for Clover to get via traditional IPO.

I… I have so many questions. Most of them are some variation of:

What the hell is going on here?

To wrap up…

Clover sounds an awful lot like a regional provider-sponsored Medicare Advantage plan that raised a bunch of VC money to build a cool tech platform to support the providers and scale the approach nationally. Unfortunately while Clover was building out the tech it has screwed up on the MA plan and tanked its quality ratings. The MA plan hasn’t demonstrated it can scale anywhere beyond New Jersey — where its friendly providers are — and Clover appears to be shifting its focus to drive future growth by becoming a tech platform / MSO for primary care docs in the nascent Medicare Direct Contracting space. That move certainly may work out well and Clover could take off in that space, but the concept seems more belief-driven than fact-driven at this point based on whats shared in the investor deck. The investor deck as a whole seems at best misleading as to current state of the business.

Oscar and Bright, for the love of god I’m begging you please file a good old fashioned S-1 with some meaningful analyses in there that we can look at with some confidence. I can’t take another GROWTH * GROWTH * GROWTH investor presentation.

In the immortal words of Jim Cramer, I’d SELL * SELL * SELL this one.